Engagement Letters for Accountants: Sample Clauses, Scope Language, and What to Never Leave Out

Quick answer: An engagement letter is contract between an accounting firm and a client that defines scope, deliverables, fees, and boundary of professional responsibility. The 8 clauses every accounting engagement letter needs are: scope of services, deliverables, fees and payment terms, responsibilities of each party, term and termination, limitation of liability, confidentiality, and signature block. Missing any one of them creates either a billing dispute or a malpractice exposure. This guide publishes real text for each clause, variations by service type, and specific scope language that prevents "but I thought you were going to do X" conversation that costs firms revenue every month.

Why most engagement letters fail

Three failure modes show up in 90% of engagement letter problems:

Vague scope language. "Bookkeeping services as agreed" is not a scope. It is an invitation for client to interpret it however benefits them, which is always broader than what you intended. The fix is named deliverables with named exclusions.

No fee structure for out-of-scope work. When client asks for "just one more thing," there is no clause that explains what that costs. So either you do it for free (margin erosion) or you have an awkward conversation (relationship damage). The fix is a defined hourly rate for work outside scope, named in letter.

Missing liability cap. The engagement letter is only place you contractually cap your liability. Without it, your exposure is your malpractice policy limit plus whatever client can argue in court. The fix is a named cap, usually equal to one year of fees.

The remaining 10% of failures are mechanical: not signed, not dated, not stored where you can find it during a dispute.

The 8 clauses every accounting engagement letter needs

This is structure that satisfies AICPA engagement letter standards and most major malpractice carriers. Each clause appears below with sample text and failure mode it prevents.

1. Scope of Services

Sample text:

Our services will be limited to following: (a) preparation of monthly financial statements consisting of balance sheet, profit and loss statement, and cash flow statement; (b) reconciliation of all bank, credit card, and merchant processor accounts on a monthly basis; (c) categorization of all transactions in QuickBooks Online against chart of accounts mutually agreed to in writing; (d) preparation of supporting workpapers retained by Firm. Our services do not include tax return preparation, payroll processing, audit, attest, or advisory services unless covered under a separate engagement letter.

Why this matters: The exclusion list is more important than inclusion list. If tax prep is not included, say so explicitly. If you are not doing payroll, say so explicitly. The phrase "unless covered under a separate engagement letter" is language that forces a new engagement (and a new fee) when client asks for additional work.

Variation by service type:

- Tax-only engagement: Replace bookkeeping deliverables with: "Preparation of Form 1040 (or applicable entity return) for tax year YYYY, including federal and state returns, based solely on information provided by Client. Our services do not include audit defense, IRS correspondence beyond initial filing, or amendments to prior-year returns."

- CFO advisory engagement: "Provision of monthly financial review meetings (60 minutes), quarterly forecast updates, and ad-hoc decision support up to 4 hours per month. Services do not include bookkeeping, tax preparation, or signatory authority on any client account."

2. Deliverables and Timeline

Sample text:

Firm will deliver following on following timeline: (a) monthly financial statements within 15 business days following end of each calendar month, subject to Client's timely provision of source documents; (b) annual W-2 and 1099 filings by January 31 of each year; (c) ad-hoc reports as requested, with reasonable lead time. Firm's delivery timeline assumes Client provides bank statements, credit card statements, and receipts within 5 business days following month-end. Delays in Client's provision of documents will result in proportional delays in Firm's deliverables.

Why this matters: Without "subject to Client's timely provision" clause, every late delivery becomes firm's fault. With it, cause is traceable to whichever party caused delay. This is single most useful clause in entire letter for protecting firm's reputation.

3. Fees and Payment Terms

Sample text:

Fees for services described in Section 1 are $X,XXX per month, billed in advance on first business day of each month, due upon receipt. Out-of-scope work will be billed at $XXX per hour, with a written estimate provided before work commences if expected to exceed 2 hours. Late payments will accrue interest at 1.5% per month. Firm reserves right to suspend services on accounts more than 30 days past due, with written notice.

Why this matters: Three protections in one clause. First, billed in advance: you are not financing client's operations. Second, named hourly rate for out-of-scope work: no debate about value billing. Third, suspension right: credible threat that prevents late-payment death spiral.

4. Responsibilities of Each Party

Sample text:

Client is responsible for: (a) maintaining adequate internal controls and safeguarding client assets; (b) providing accurate and complete information to Firm; (c) reviewing all deliverables and notifying Firm of errors within 30 days of delivery; (d) making all financial decisions; (e) compliance with all federal, state, and local tax filing obligations not specifically included in Section 1. Firm is responsible for: (a) performing services described in Section 1 with reasonable professional care; (b) maintaining confidentiality of Client information; (c) complying with applicable AICPA professional standards and AICPA Code of Professional Conduct.

Why this matters: The asymmetry is intentional. The client's responsibilities are extensive because most disputes start with client failing one of them. The firm's responsibilities are narrow because standard of care is "reasonable professional care" not a guarantee of perfection.

5. Term and Termination

Sample text:

This engagement begins on [date] and continues until terminated by either party with 30 days written notice. Firm may terminate immediately for non-payment, material breach by Client, or discovery of facts indicating fraud or illegal activity. Upon termination, Client will pay all fees through date of termination. Firm will return all Client documents within 30 days, retaining workpapers as required by professional standards.

Why this matters: The "may terminate immediately for fraud" language is protection that lets you exit a client engagement cleanly when something illegal surfaces. Without it, exiting under those circumstances becomes a contractual breach risk for firm.

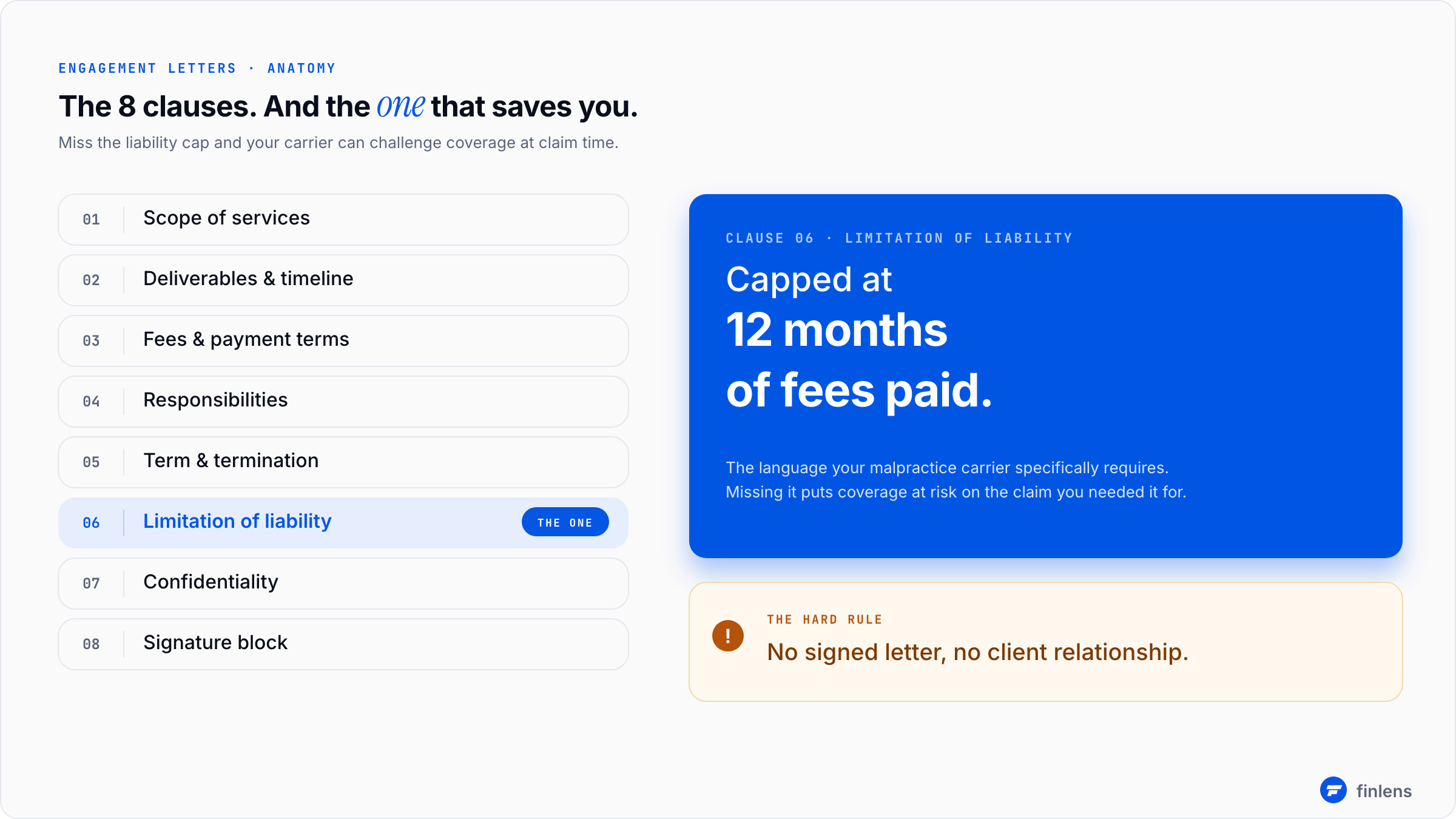

6. Limitation of Liability

Sample text:

The total cumulative liability of Firm for any claim arising out of or related to this engagement, whether based on contract, tort, negligence, strict liability, or otherwise, shall not exceed total fees paid by Client to Firm during 12 months immediately preceding event giving rise to claim. In no event shall Firm be liable for consequential, incidental, indirect, punitive, or special damages.

Why this matters: This is clause your malpractice carrier specifically requires. Most carriers including CAMICO and AON publish required language that has to appear in every engagement letter to maintain coverage. If you do not include this language, a claim that would have been covered may be denied because underlying engagement was uncapped.

Check with your malpractice carrier for their specific required text. Most have a downloadable engagement letter addendum that should be incorporated verbatim.

7. Confidentiality

Sample text:

Each party will maintain confidentiality of other party's confidential information and will not disclose it to any third party without written consent, except as required by law, court order, or regulatory subpoena. Firm may disclose Client information to its employees and contractors who have a need to know, subject to confidentiality obligations. Client information may be used in anonymous, aggregated form for Firm's internal benchmarking and quality improvement purposes.

Why this matters: The "anonymous, aggregated" carve-out is language that lets firm use client data for benchmarking and AI training without violating confidentiality. Modern engagement letters need this to be explicit because AI tools may process client data in ways that 2015-era language did not contemplate.

8. Signature Block

Sample text:

By signing below, parties acknowledge they have read, understood, and agreed to terms of this engagement letter.

Client: ___________________ Date: ___________ Firm: ____________________ Date: ___________

Why this matters: Sounds obvious. Engagement letter disputes routinely involve unsigned letters. If client never signed, contract is harder to enforce. The fix is a system that does not advance to onboarding stages 2+ until signed letter is in hand.

Tax engagement letter additions

Tax engagements need two additional clauses beyond standard 8:

IRS authorization language.

Client authorizes Firm to receive Client's tax information from Internal Revenue Service under Form 8821 (Tax Information Authorization). Client further authorizes Firm to represent Client before IRS under Form 2848 (Power of Attorney) if specifically agreed to in writing. This engagement does not include audit defense, examination representation, or correspondence with IRS beyond submission of prepared return, unless covered under a separate engagement letter.

Circular 230 acknowledgment.

Firm is subject to standards of practice set forth in Treasury Department Circular 230, governing practice before IRS. Firm will exercise due diligence in preparing Client's returns and will rely on information provided by Client in good faith. Firm is not responsible for verifying accuracy or completeness of information provided.

This second clause is language that limits firm exposure when a client provides false or incomplete information. The AICPA Statement on Standards for Tax Services (SSTS) governs specific diligence standard.

Bookkeeping engagement letter additions

For bookkeeping-only engagements, add an explicit "we are not auditors" disclaimer:

Firm's services do not include an audit, review, or compilation of Client's financial statements. The financial statements prepared by Firm are based on information provided by Client and are not subject to independent verification. Client is responsible for accuracy and completeness of all source documents. Firm does not provide assurance on financial statements.

This clause is what prevents a client from later claiming that books had implicit audit-level assurance. Without it, "I thought you were checking" becomes a defensible position for a client in a dispute.

Scope creep prevention: language that works

The single highest-leverage clause is one that defines what happens when client asks for something not in original scope. The boilerplate "out-of-scope work billed at $X/hour" is necessary but not sufficient. Stronger language:

Any request from Client for services outside scope described in Section 1 will be considered a separate engagement. Firm will provide a written estimate of fees and timeline before commencing such work. No out-of-scope work will be performed without Client's written authorization of estimate.

The phrase "no out-of-scope work will be performed without written authorization" is what changes behavior. Without it, firm absorbs scope creep. With it, every additional ask triggers a small, explicit moment where client either authorizes additional fee or withdraws request. Most withdraw.

Common mistakes that void engagement letters

Five patterns kill engagement letters in practice:

1. Using same letter for every service type. A bookkeeping engagement and a tax engagement need different scope language, different responsibilities, and different liability caps. Force additional 30 minutes to customize.

2. Sending it after work has started. An engagement letter signed after work began is harder to enforce than one signed before. The order is: scoping conversation → engagement letter → countersignature → work begins. Not other way around.

3. Missing malpractice carrier's required language. Verify with your carrier. Their required clauses must appear verbatim or coverage can be challenged at claim time.

4. Auto renewing without an update window. Engagement letters that auto-renew annually without an update step calcify outdated scope. Build in a 30-day pre-renewal review where both parties can adjust scope before next term begins.

5. Not storing signed copies systematically. A signed engagement letter that nobody can find during a dispute is functionally unsigned. Store in a system whole firm can access, indexed by client name and engagement type.

Frequently asked questions

How often should I update my engagement letter template?

Annually at minimum, plus whenever your services change materially or your malpractice carrier publishes new required language. Most firms do an annual review in November or December to prepare for new year's engagements.

Do I need a separate engagement letter for every service I provide to same client?

Yes if services are materially different (tax vs. bookkeeping vs. advisory). Yes if malpractice carrier requires it. Many firms run separate letters for bookkeeping engagement and annual tax engagement even when same client, because scope and liability profile differ.

Can I email an engagement letter or does it need to be a physical signature?

Electronic signatures are valid under federal law (E-SIGN Act) and in every US state under Uniform Electronic Transactions Act. Most firms use DocuSign, Adobe Sign, or built-in e-sign in their practice management software. Physical signatures are not required.

What happens if client refuses to sign?

The client does not become a client. Hard rule. Firms that advance to onboarding stages 2+ without a signed engagement letter create both legal exposure and a precedent that firm's process is negotiable. Walk away.

Does engagement letter need to mention my software stack?

Generally no, but confidentiality section should cover how client data is handled in third-party systems. Modern engagement letters reference cloud accounting software (QuickBooks Online) and any AI or automation tools (Finlens, Karbon) under data handling provisions. This is most important for tax engagements where client SSNs and other PII flow through multiple systems.

Where does engagement letter fit in broader client onboarding workflow?

It is Stage 1 deliverable in a standard accounting firm onboarding system. The signed letter is exit criterion that triggers Stage 2 (kickoff call and authorizations).

Can I use AICPA template directly?

Yes, and most firms should start there. The AICPA engagement letter resources include service-specific templates. Customize scope and fee sections for your firm, then add your malpractice carrier's required language.

An engagement letter is a 4-page document that prevents 4 different categories of failure. Most firms try to skip this work or copy a template they have not read carefully. The cost of doing it right is one weekend of careful drafting plus annual updates. The cost of doing it wrong shows up in scope creep, billing disputes, denied malpractice claims, and conversation with a client where neither party can prove what was agreed.

For broader operational system this letter sits inside, client onboarding covers 5-stage workflow that turns a signed engagement letter into a fully operational client file. For firms past 30 clients, practice management software comparison covers tools that store engagement letters where whole firm can find them.