Is Revenue a Debit or Credit? A Clear Guide for Accountants

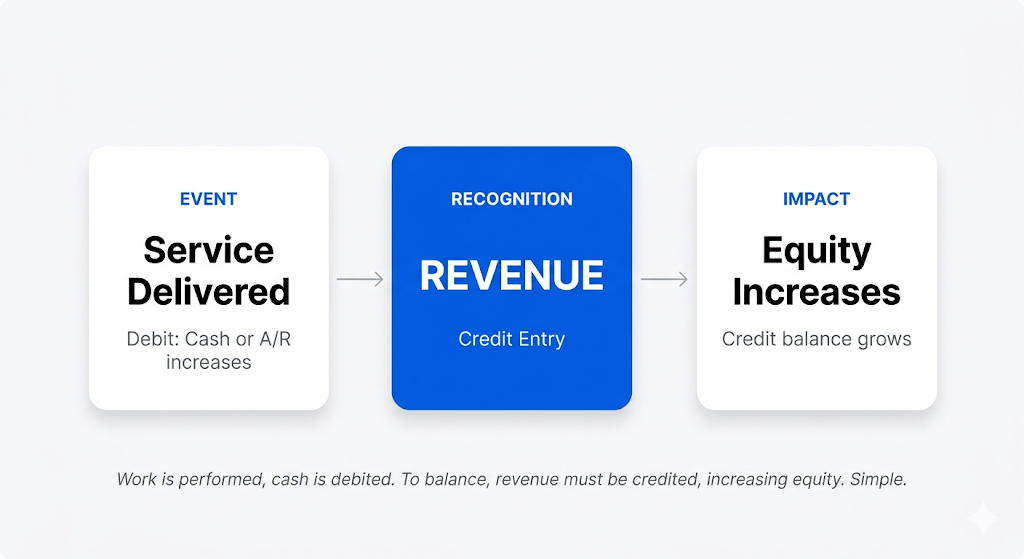

Revenue is a credit. When a business earns revenue, you record it as a credit because it increases owner's equity on right side of accounting equation. The matching debit goes to an asset account like cash or accounts receivable. This is foundation of double entry bookkeeping, and getting it wrong creates problems that ripple through every financial statement you produce.

If you manage multiple clients, you already know this. But real challenge is not remembering rule. It is applying it consistently across dozens of accounts, hundreds of transactions, and tight month end deadlines. That is exactly kind of problem we built Finlens to solve.

Why Is Revenue Recorded as a Credit?

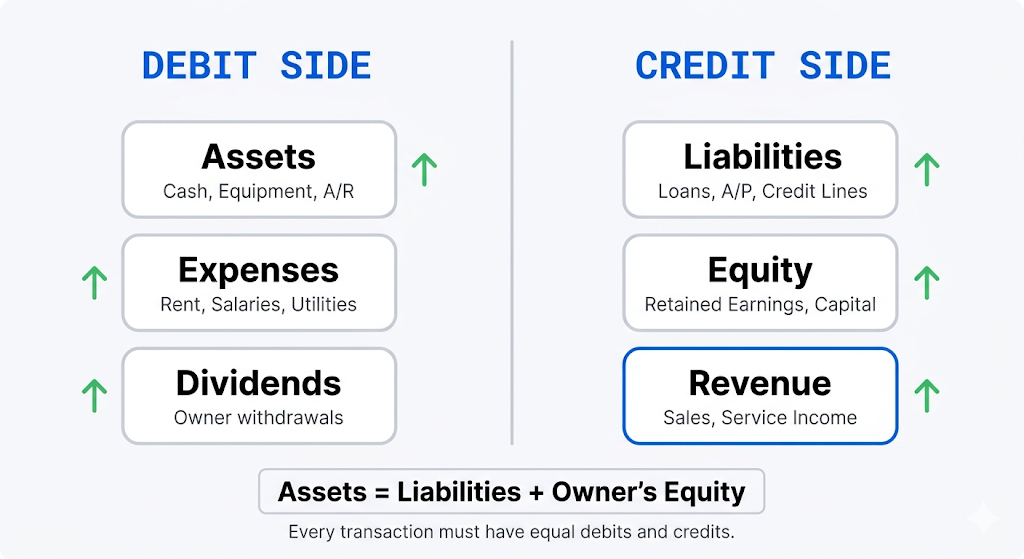

Revenue is a credit because of accounting equation: Assets = Liabilities + Owner's Equity. Revenue increases the owner's equity, which sits on right side of equation. In double entry bookkeeping, increases to right side accounts are always credits.

Here is logic broken down simply. When a business earns money, two things happen at once. An asset grows (cash comes in or a receivable is created), and equity grows (business is now worth more). The asset increase is a debit. The equity increase, through revenue, is a credit. Both sides stay balanced.

Quick reference: Revenue accounts carry a normal credit balance. A debit to a revenue account decreases it. This matters when you record returns, discounts, or adjustments.

Are Expenses a Debit or Credit?

Expenses are debits. They decrease owner's equity, so they go on opposite side from revenue.

When a business pays rent, buys supplies, or covers payroll, you debit expense account and credit cash or accounts payable. The expense reduces equity, cash outflow reduces assets, and equation stays balanced.

This is where many bookkeeping errors start. If you accidentally credit an expense account instead of debiting it, income statement overstates profit. Multiply that across 20 or 30 client accounts, and you are looking at serious cleanup work during close. If you are still automating monthly journal entries in QuickBooks manually, these errors happen more often than they should.

Debit vs. Credit: The Complete Account Type Breakdown

Instead of memorizing isolated rules, use this table as a single reference for how debits and credits behave across all five core account types.

A helpful way to remember this is DEALER framework: Dividends, Expenses, and Assets are debit normal. Liabilities, Equity, and Revenue are credit normal. Every transaction needs at least one debit and one credit, and totals must match. If they do not, something is wrong.

How Revenue Entries Actually Work (With Examples)

Theory is useful. Let's look at how this plays out in real bookkeeping.

Example 1: Cash sale. A consulting firm bills a client $5,000 and gets paid immediately. You debit Cash for $5,000 and credit Service Revenue for $5,000.

Example 2: Sale on credit. The same firm completes work but client will pay in 30 days. You debit Accounts Receivable for $5,000 and credit Service Revenue for $5,000. When the client pays, you debit Cash and credit Accounts Receivable.

Example 3: Revenue adjustment. The client disputes $500 of invoice. You debit Service Revenue (or a Sales Allowances account) for $500 and credit Accounts Receivable for $500. The revenue account balance goes down.

Here is a quick summary of how each entry flows:

These entries are straightforward in isolation. They get complicated when you are handling them for multiple clients with different revenue recognition timing, chart of accounts structures, and reporting periods.

Where Accrual Accounting Makes This Harder

If your clients use accrual accounting (and most businesses above a certain size do), you record revenue when it is earned, not when cash arrives. This creates timing gaps that make credit or debit accounting entries more complex.

Consider a common scenario. Your client delivers a $10,000 project in March but does not receive payment until May. Under accrual accounting, you book revenue in March: debit Accounts Receivable $10,000, credit Revenue $10,000. In May, when payment arrives, you debit Cash and credit Accounts Receivable.

Now multiply this across a client base where some invoices span multiple months, some payments arrive in partial amounts, and some revenue needs to be deferred. You are now tracking dozens of timing entries, each needing correct debit credit pair.

This is where most manual bookkeeping breaks down. Not because accountant does not understand rules, but because volume creates opportunities for errors that are hard to catch until month end.

The overlooked problem: Most firms catch accrual errors during close process, which means they spend first week of every month fixing last month's books instead of doing advisory work. We built Finlens specifically for this. It automates accrual entries and reconciliation on top of QuickBooks, so books are clean before month end even starts. No migration, no new ledger. You keep your existing QuickBooks setup and layer our AI automation over it. If you want to see this in action, check out how Finlens automates accrual journal entries.

For a solid primer on fundamentals of credits and debits in bookkeeping, GBQ's guide to understanding debits and credits walks through core concepts with clear examples.

What Happens When Debits and Credits Are Wrong?

Misclassified entries do not always show up as obvious errors. The books might still balance technically, but financial statements tell wrong story. Here is what goes wrong.

Revenue credited to wrong account skews income reporting. A service revenue entry posted to "other income" changes revenue mix on P&L and misleads client about where their money comes from.

Expenses debited to an asset account inflate the balance sheet. The client thinks they have more assets than they do, and expenses look artificially low.

Reversed entries (debiting revenue instead of crediting it) understate income. If this happens near period end, it throws off tax estimates and financial projections.

For accountants managing client books, these errors do not just create rework. They erode client trust. When a client gets a financial report that does not match their bank account reality, they start questioning everything.

How to Reduce Entry Errors Across Multiple Clients

If you are handling bookkeeping for more than a handful of clients, answer is not "be more careful." The answer is to reduce number of manual entries you make.

Before Finlens: You log into QuickBooks for each client, review bank feeds, manually categorize transactions, post journal entries for accruals and adjustments, reconcile accounts, and then run reports. Repeat for every client, every month.

After Finlens: Our AI sits on top of QuickBooks and handles categorization, reconciliation, and accrual entries automatically. You review and approve instead of building entries from scratch. The debit credit pairs are pre mapped, accruals are tracked in real time, and exceptions are flagged before they become month end problems.

The difference is not just speed. It is margin. Every hour you save on manual entry work is an hour you can spend on advisory services or onboarding another client. And at $49/month with a free forever tier available, math works even for solo practitioners.

Revenue Recognition and Credit Entries Under Different Methods

How you credit revenue depends on your client's accounting method.

Cash basis: Revenue is credited when payment is received. Simple and straightforward, but it does not reflect actual business performance in any given period.

Accrual basis: Revenue is credited when earned, regardless of when cash arrives. More accurate, but requires careful tracking of receivables and deferred revenue.

Modified cash basis: A hybrid where some transactions follow accrual rules and others follow cash rules. This creates even more complexity in determining when to credit revenue.

For accountants, challenge is that different clients may use different methods. You need to know rules for each and apply them correctly across every engagement. This is another area where standardized workflows and automation pay off quickly. If you deal with deferred revenue schedules regularly, we have a separate walkthrough on automating deferred revenue recognition for SaaS on QuickBooks that covers specifics.

FAQ

1. Is revenue a debit or credit?

Revenue is a credit. It increases owner's equity, which carries a normal credit balance. When a business earns revenue, you credit revenue account and debit an asset account like cash or accounts receivable.

2. Are expenses a debit or credit?

Expenses are debits. They decrease owner's equity, so they are recorded on debit (left) side. You debit expense account and credit cash or accounts payable.

3. Why does revenue have a credit balance?

Revenue has a credit balance because it flows into owner's equity, which sits on right side of accounting equation (Assets = Liabilities + Owner's Equity). Increases to right side accounts are credits.

4. What is difference between debit and credit in accounting?

A debit increases assets, expenses, and dividends. A credit increases liabilities, equity, and revenue. Every transaction requires at least one debit and one credit that are equal in value.

5. How do you record revenue in a journal entry?

Debit asset account (cash or accounts receivable) for amount earned. Credit revenue account for same amount. Both entries must match to keep books balanced.

6. Does a debit to revenue increase or decrease it?

A debit to revenue decreases it. Revenue carries a normal credit balance, so debits reduce balance. You would debit revenue when recording returns, allowances, or adjustments.